📊 Cybersecurity Funding Review - November 2022

Cybersecurity Funding Review - A look back at what moved the cybersecurity market in November 2022.

It's that time again.

Each month I do a recap on the business of cybersecurity funding and M&A news by the numbers, with visuals, and with my own commentary. I tweak these reports month-to-month based on feedback I get from readers like you, so let me know what I should start, stop, or continue.

I build these reports each month from some the data I collect each week from the Security, Funded newsletter. If you're interested in poking through a different slice of the data, check out the Cybersecurity VC Database I made.

If you're not signed up yet, make sure you get in on the best, most reliable, and detailed resource for cybersecurity investing and M&A news on the Internet. 👇

By the Numbers

A look at what moved the private cybersecurity market in November 2022 by the numbers.

- Approximately $906.0M was invested in 46 cybersecurity companies across 32 unique product categories in October 2022, down less than half from the $2.1B in October 2022.

- 27 companies across 13 unique product categories were acquired or had a merger event to the tune of $195.0M in publicly available data.

- Series B events saw the highest funding at $389.4M

- ~64% of funding went to United States-based companies

My Thoughts and Predictions

- The Remote Browser Isolation category continues to see huge rounds and we get a glimpse into what later-stage future funding might look like in this macro-economic-depressed state. I've mentioned how investors in 2022 seemed to treat Password Managers and Remote Browser Isolation companies the same way before, but that looks likely to change in 2023.

Shoutout to @Bitwarden @1Password pic.twitter.com/ZYxNblJeVO

— Mike Privette (@mikepsecuritee) September 8, 2022

- The Web3 industry continued its trend of funding specific to that sector. Following on the heels of continued breaches, scams, and Ponzi schemes, this space can't get regulation and oversight to protect investors and consumes quickly enough.

- It's interesting that more deals and funding went private (meaning the investors weren't named publicly) than any other time this year. This could mean that investors are being more cautious with their deals, that down round investments are happening (selling shares or company equity at a lower valuation than before causing ownership dilution), or it could mean nothing at all and just be a ghost in the machine.

- November was compounded on a few fronts that I believe led to a lower volume of funding. It was the most recent height (or low depending on how you look at it 🤔) of macroeconomic fears and low investor sentiment in general. Investors took a bit more time for due diligence or to be more selective and Thanksgiving also happened in the US, which drives the most volume globally.

- I expect an uptick in deal sizes, volume of deals, or both as investors squeeze things in before the new year.

- As I said last month, buyers are still cashed strapped like last month and will be for the rest of 2022 and into 2023. This makes it harder for startups to show traction and get the proof that investors need of their true product market fit.

Funding Events by Round

- 16 Seed round events equal to $81.4M

- 8 Series B round events equal to $389.4M

- 6 Venture Round round events equal to $90.5M

- 5 Series A round events equal to $71.9M

- 3 Series C round events equal to $75.0M

- 2 Private Equity round events equal to $36.0M

- 2 Pre-Seed round events equal to an undisclosed amount

- 2 Grant round events equal to $25.0K

- 2 Debt Financing round events equal to $161.5M

Top 5 Funding Events

- Giesecke+Devrient, a Germany-based managed security services provider (MSSP), raised a $135.0M Debt Financing round. (more)

- Apiiro, an application and supply chain security platform, raised a $100.0M Series B from General Catalyst. (more)

- TRM Labs, an anti-fraud platform for cryptocurrencies and Web3, raised a $70.0M Series B from Thoma Bravo. (more)

- Akeyless Security, an Israel-based secrets management platform, raised a $65.0M Series B from ngp capital. (more)

- Island, a secure remote browser isolation platform, raised a $60.0M Series B from Georgian. (more)

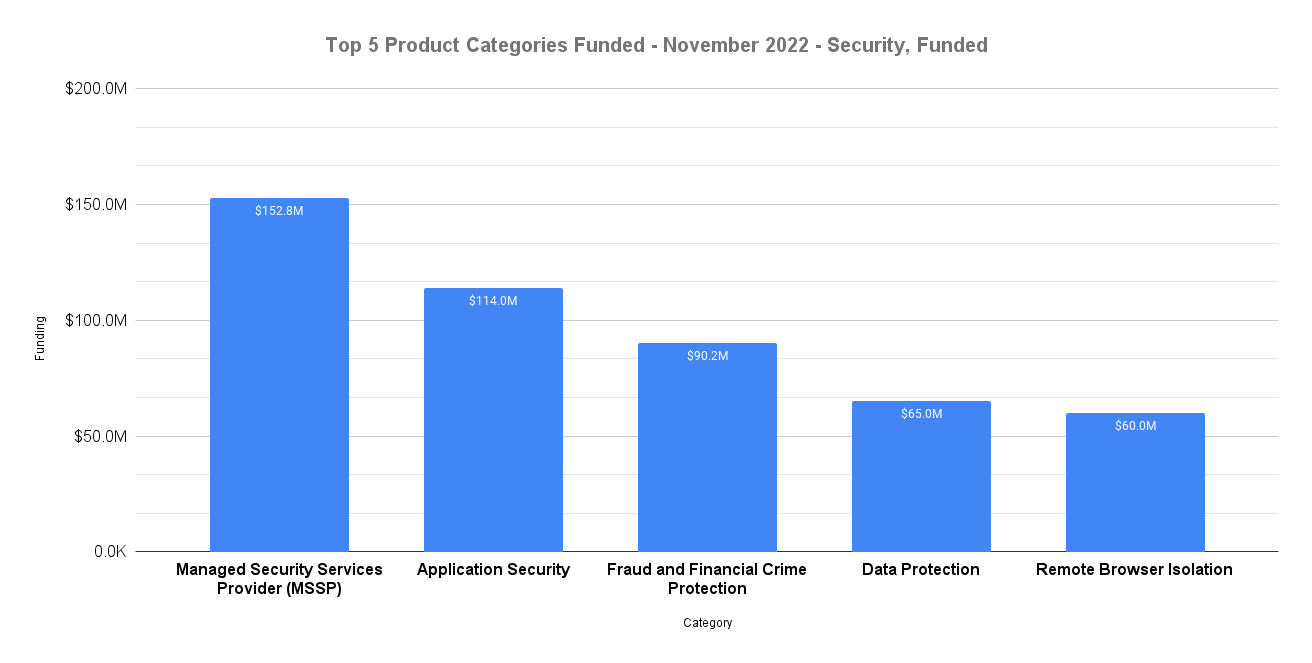

Top Funded Product Categories

- $152.8M for Managed Security Services Provider (MSSP)

- $114.0M for Application Security

- $90.2M for Fraud and Financial Crime Protection

- $65.0M for Data Protection

- $60.0M for Remote Browser Isolation

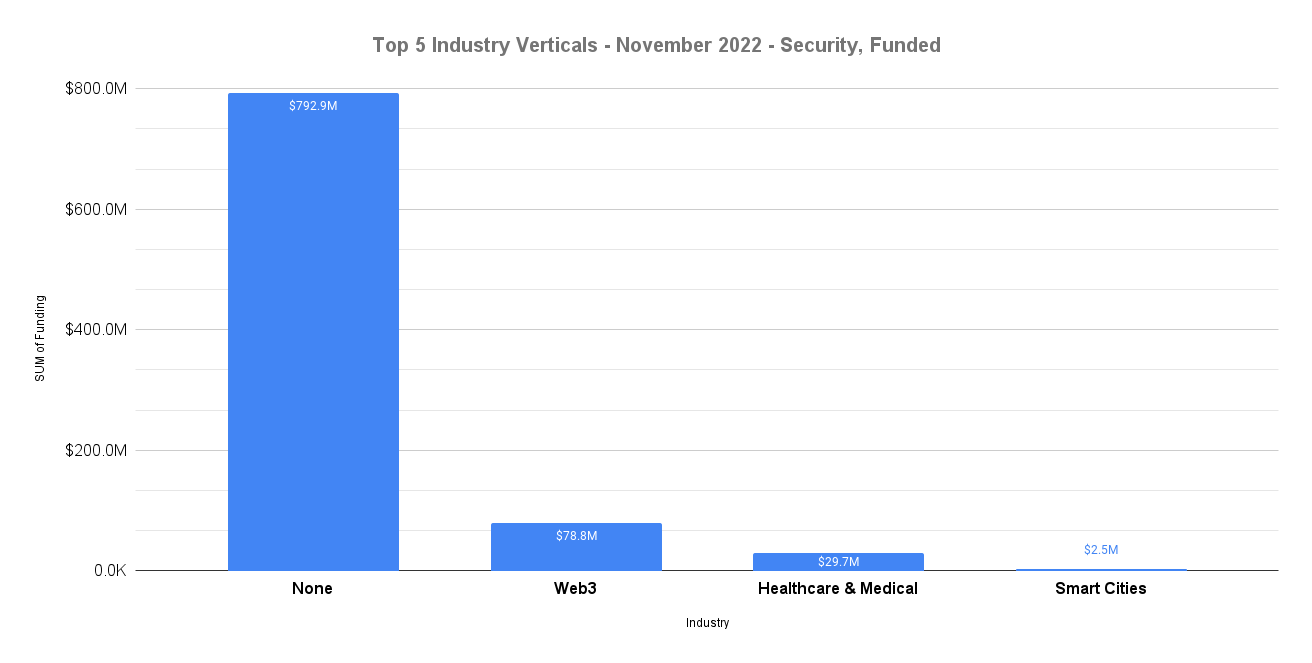

Top Funded Industries

- $792.9M was not industry specific

- $78.8M for Web3

- $29.7M for Healthcare & Medical

- $2.5M for Smart Cities

- $1.9M for Telecommunications

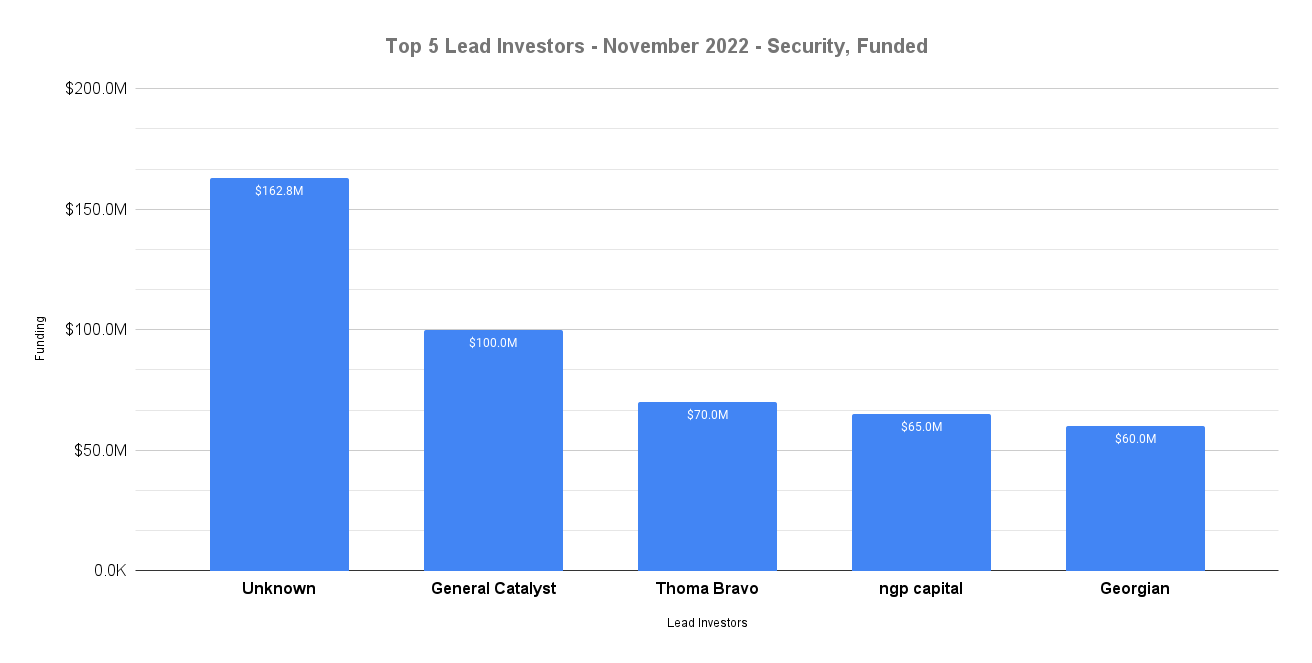

Top Lead Investor Teams

- $162.8M for unnamed investors across several deals

- $100.0M for General Catalyst

- $70.0M for Thoma Bravo

- $65.0M for ngp capital

- $60.0M for Georgian

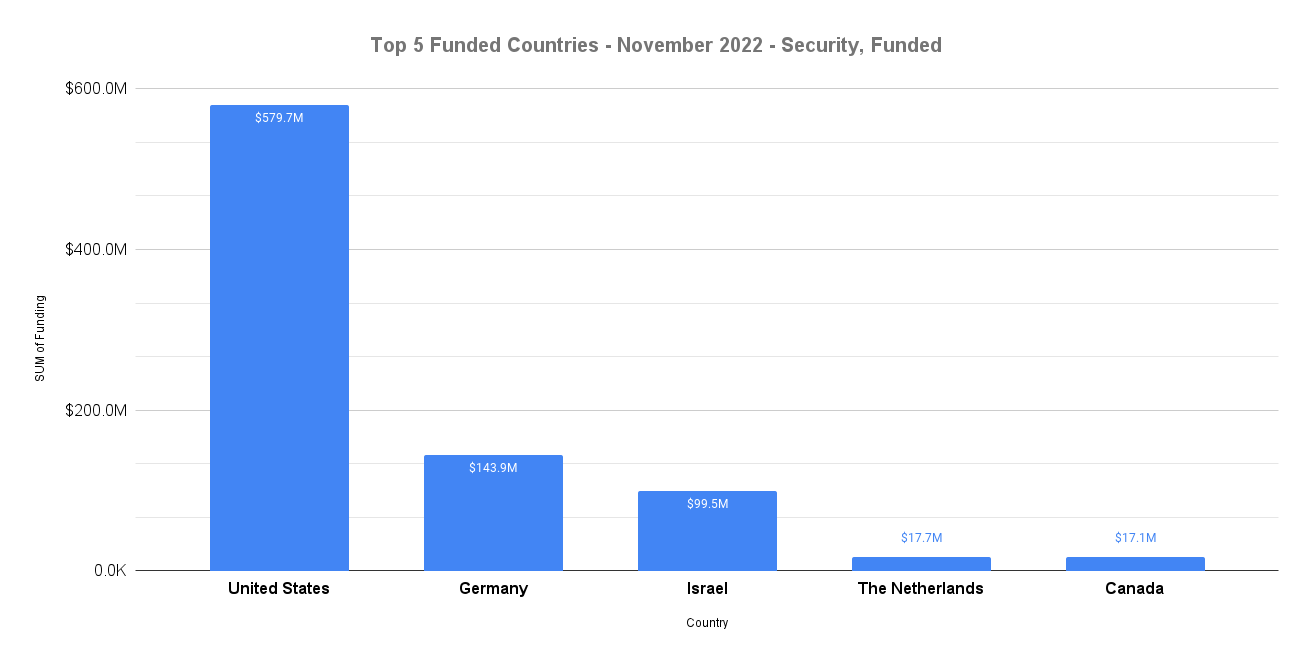

Top Funded Countries

- $579.7M for United States 🇺🇸

- $143.9M for Germany 🇩🇪

- $99.5M for Israel 🇮🇱

- $17.7M for The Netherlands 🇳🇱

- $17.1M for Canada 🇨🇦

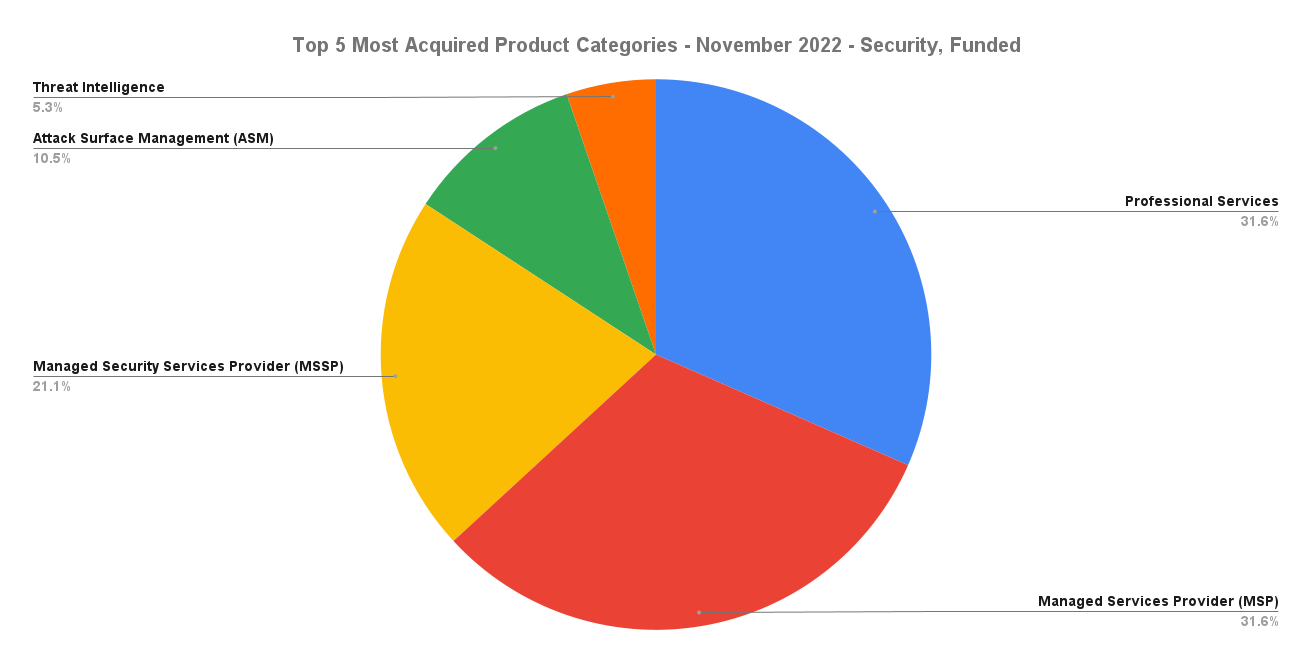

Top Acquired Product Categories

Data Collection Methodology

A few tenants I follow for collecting and creating this data:

- I only use public data sources

- I evaluate each company that makes this list to make sure they are actually solving a cybersecurity problem

- I personally assign the product category for each company (regardless of what the marketing says)

- All monetary values are in U.S. dollars and currencies are converted, if needed, at the time of collection

- All monetary values are from the time of collection

Wrapping Up

If you like a chart, statement, or prediction I made, let me know. If you want me to dig in further on something or see the data sliced in a different way, let me know.

Likewise, if you don't like something or if something doesn't make sense, let me know. I do this to contribute something new and add value to the industry so I want to make sure I'm also taking feedback.

See you again next month!

Cheers,

Mike P