📊 Cybersecurity Funding Review - July 2022

Cybersecurity Funding Review - A lookback at what moved the cybersecurity market in July 2022.

Each month I do a quick recap of cybersecurity funding and acquisition stats by the numbers with visuals.

All of this is built off of the data I collect each week from the Security, Funded newsletter.

If you're not signed up yet, make sure you get in on the most reliable and detailed resource for cybersecurity investing news on the Internet.

Subscribe to Security, Funded

Know what's moving the market in cybersecurity.

At a Glance by the Numbers

A lookback at what moved the cybersecurity market in July 2022 by the numbers

- Approximately $1.2B was invested in 34 cybersecurity companies across 25 unique product categories in July 2022, a healthy rebound from the $919.6M in June 2022, but with 37% fewer companies down from 54.

- ~50% of funding from July came from just 3 transactions to the tune of $600.0M

- Over 60% of funding went to United States-based companies, a 10% drop from June 2022, with over 20% of funding going to Switzerland-based companies.

- 21 companies across 11 unique product categories accounted for $126.3M merger or acquisition events, a significant drop from publicly available data of $700.0M in June 2022

- Professional Services companies were the most acquired category of company, followed by Managed Security Services Providers (MSSPs).

My Anecdotes

- This bit of "rebounding" in July shows the continued resiliency in the cybersecurity market.

- The VC and PEGs who major in cybersecurity will continue to reap the rewards of their efforts as those who only dabble in cyber will take a conservative step back.

- The companies who can still raise at favorable valuations will the day and those who cannot will be targets for M&A.

- M&A is still on a tear this year (and will continue to be) in the cybersecurity market as larger players look to add depth to their existing portfolio of capabilities.

- This level of consolidation will ultimately drive better innovation is the sub-markets within cybersecurity come closer together. It's either that or be stifled out, and that's simply not something cybersecurity founders and their VC backers do.

- The Web3 and cybersecurity collision is coming (and is long overdue). July saw more security-related funding in the Web3 – crypto, NFTs, blockchains, distributed ledger technology (DLT) – than any other month yet. This is just the tip of the iceberg in this space.

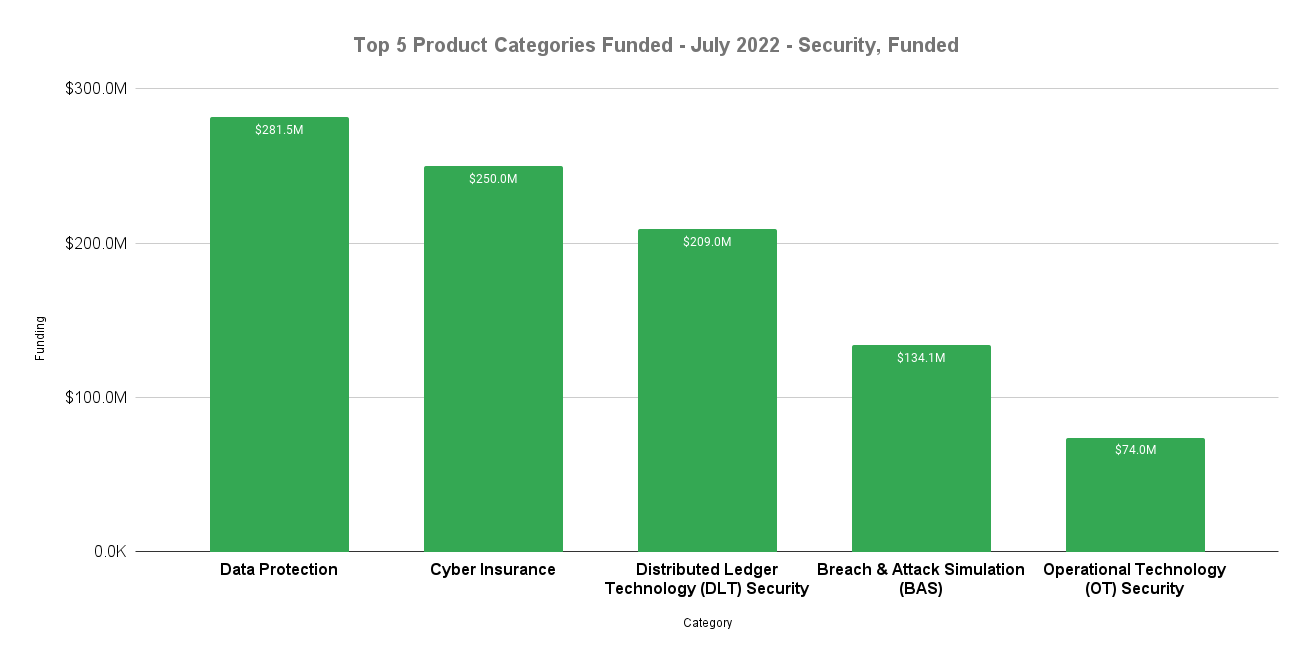

Top Funded Product Categories

- $281.5M for Data Protection

- $250.0M for Cyber Insurance

- $209.0M for Distributed Ledger Technology (DLT) Security

- $134.1M for Breach & Attack Simulation (BAS)

- $74.0M for Operational Technology (OT) Security

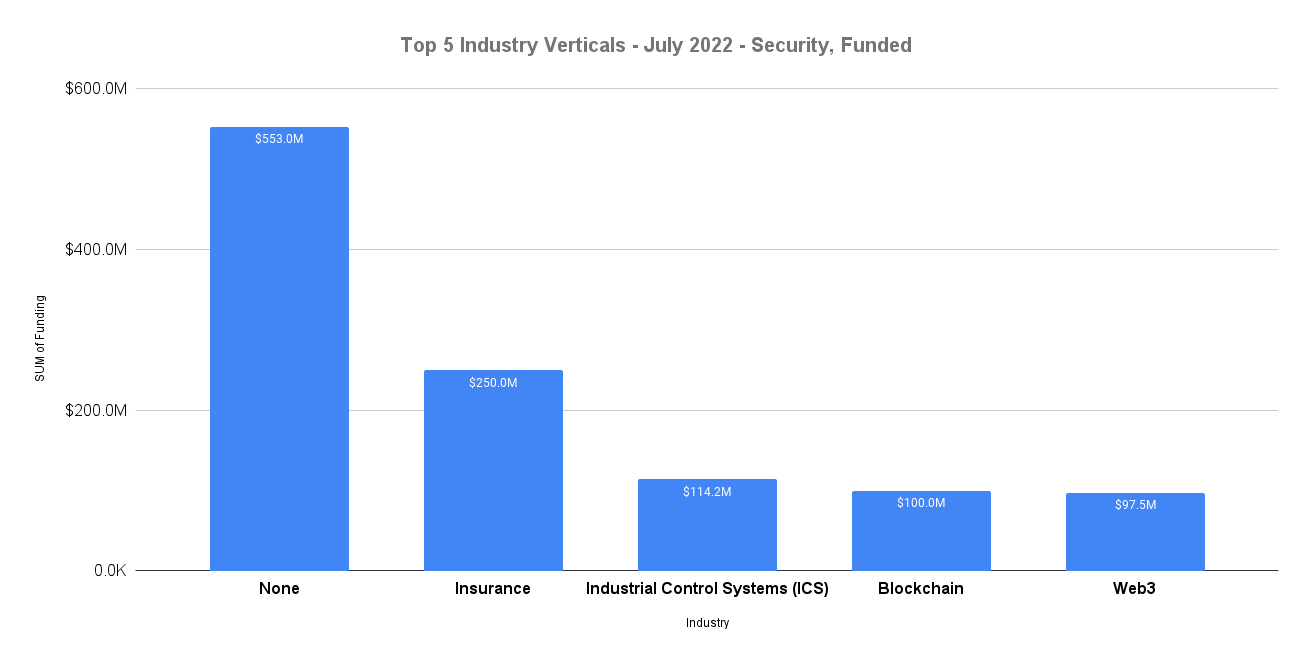

Top Funded Industries

- $553.0M for No Specific Industry

- $250.0M for Insurance

- $114.2M for Industrial Control Systems (ICS)

- $100.0M for Blockchain

- $97.5M for Web3

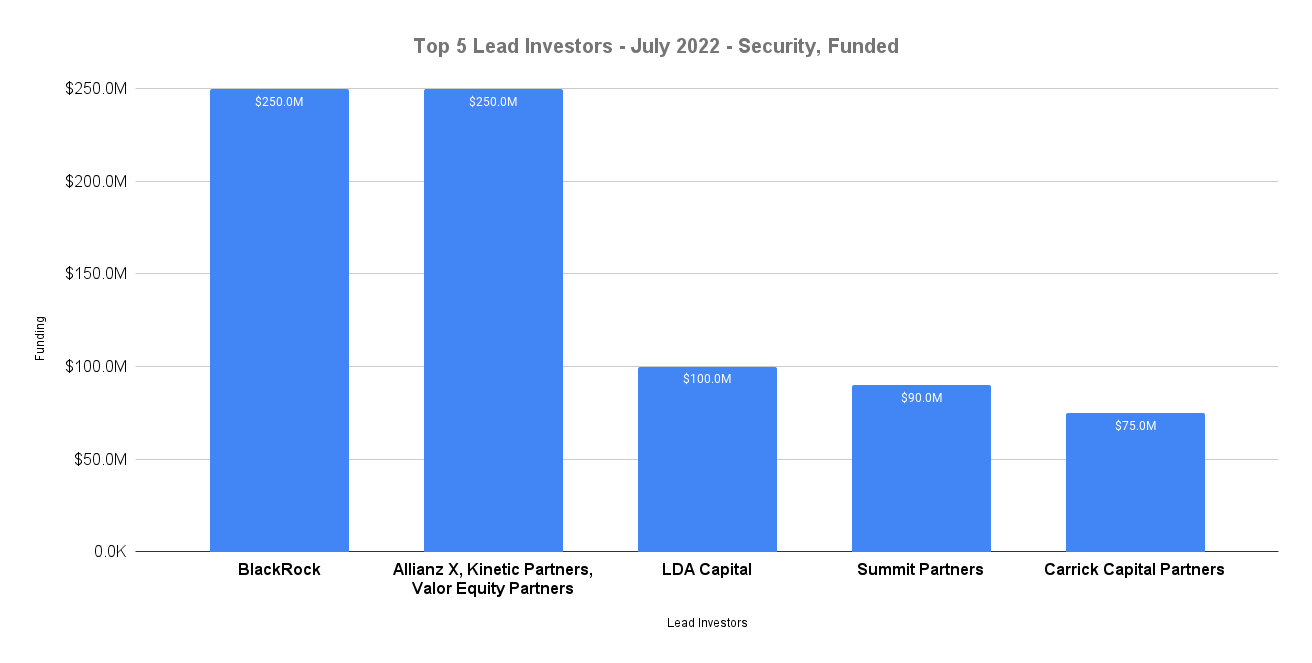

Top Lead Investor Teams

- $250.0M from BlackRock

- $250.0M from Allianz X, Kinetic Partners, Valor Equity Partners

- $100.0M from LDA Capital

- $90.0M from Summit Partners

- $75.0M from Carrick Capital Partners

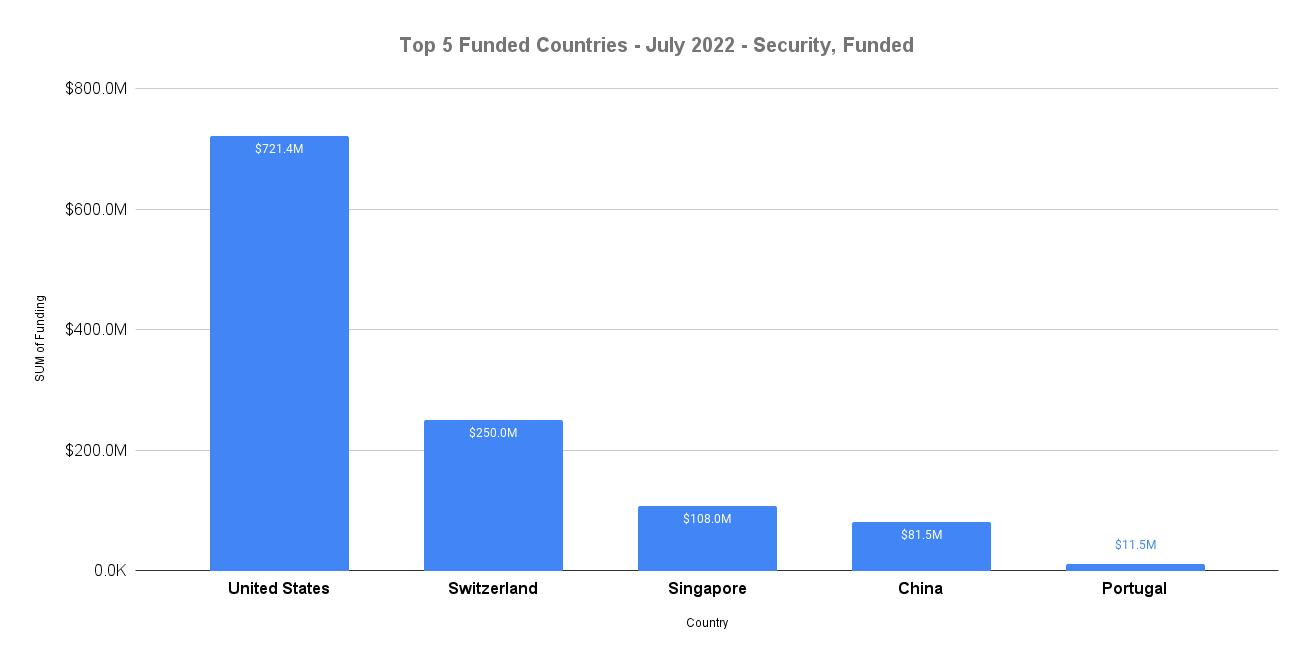

Top Countries Funded

- $721.4M for United States

- $250.0M for Switzerland

- $108.0M for Singapore

- $81.5M for China

- $11.5M for Portugal

Data Collection Methodology

A few tenants I follow for collecting and creating this data:

- I only use public data sources

- I evaluate each company that makes this list to make sure they are solving a cybersecurity problem

- I personally assign the product category for each company (regardless of what their marketing says)

- All funding and acquisition values are in U.S. dollars

- All funding amounts are from the time of collection

Go Deeper

Do you want to get access to the data I collect every month so you can do additional analysis?

Just want the data delivered to you every week without having to do the heavy lifting yourself?

I've got you! Check out the data subscription service to learn more.

Cheers,

Mike P